Embedded Fintech and Payment Innovation: Why Quality and Testing Matter

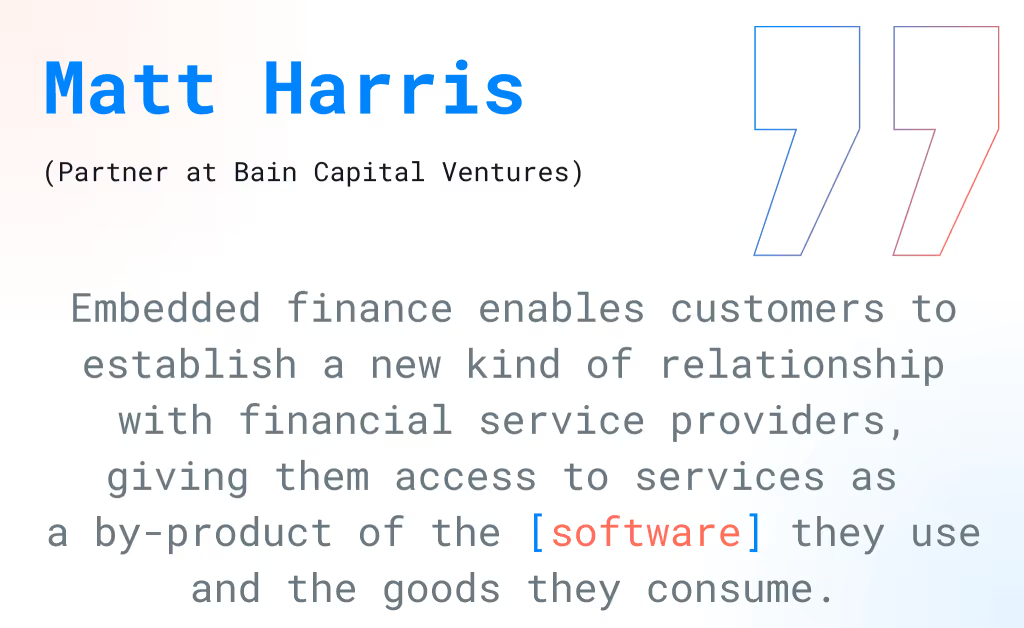

Embedded Systems are specialized electronic components designed to perform specific functions within larger systems – drive the development of financial services like mobile payments (including BNPL) and banking process automation to risk and data security management. "Embedded finance is the integration of financial services into non-financial offerings. Examples of embedded finance include an e-commerce retailer providing insurance, a coffee shop app enabling one-click payments, or a branded credit card from a department store." – said Tom Sullivan, The Director of Product at Plaid. However, as technology advances, the need for maintaining the highest quality and security standards for these systems also grows.In this article, we will examine how superiority and testing fuel innovation in fintech, the challenges faced by companies implementing embedded systems, and why testing is essential for building user trust and ensuring the long-term market value of financial products.

Examples of Embedded Finance in Cashless Payment Systems and POS Terminals

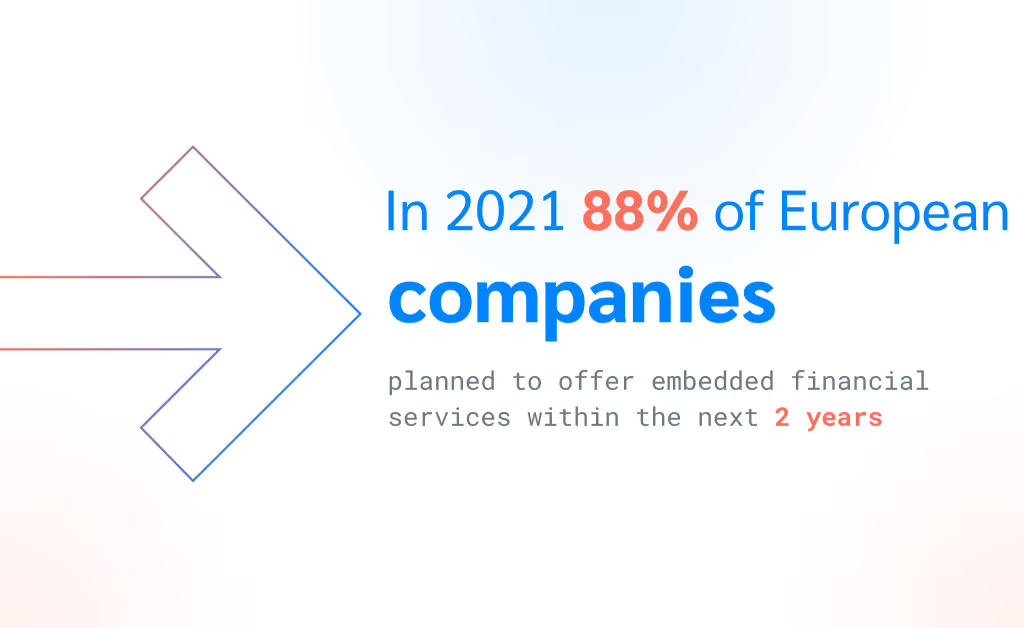

Based on embedded systems, modern payment terminals streamline fast and secure transactions with cards or mobile devices. POS terminals have dedicated microprocessor units that perform authorization operations and process payments in real time. These devices have undergone significant evolution with the integration of financial sector, and their functionality now extends far beyond simple transaction handling. According to Statista Research Department in 2021, 88% of European companies planned to offer embedded financial services within the next two years, indicating growing interest in this business model. One of the key technologies used in contactless payments is NFC (Near Field Communication), which allows transactions to be completed via short-range communication between devices (e.g., a POS terminal and a card or smartphone).Integration with mobile payment apps like Google Pay, Apple Pay, and Samsung Pay accelerates the shift to a cashless future. Embedded-system-equipped POS terminals can support mobile payments, carried out using virtual payment cards stored on mobile devices.Modern POS terminals can connect with other devices, such as cash registers or inventory systems, through Bluetooth and Wi-Fi. They can also be integrated with cloud services, allowing transaction data to be transmitted in real-time to central databases.

From Hardware to Software: The Structure of Embedded Payment Systems in ATMs

Nowadays, ATMs are complex devices where embedded systems integrate various modules, working together to ensure smooth operation. The fundamental components include:

Processor Module: At the heart of every ATM is a microprocessor that manages all communication with the bank, processes customer data, and executes user commands. The processor works with embedded software to enable seamless command processing, transaction authorization, and control of other components.

Scanning and Security Modules: Modern ATMs use embedded systems responsible for card and PIN scanning as well as biometric authorization. These systems communicate in real-time with the bank or an external authentication system to verify user identity.

Payment Modules: The modules responsible for cash handling, such as deposits and withdrawals, are essential in every ATM. Embedded systems allow for sorting banknotes, verifying their authenticity, and securely storing cash within the device.

Power Management Systems: With embedded systems, ATMs can save energy in standby mode while quickly responding to user requests. Energy-efficient circuits also enable faster resumption of operation after switching from sleep mode.

Customer Experience in Action: Top Applications in Self-Service Embed Financial Terminal

Self-service financial machine use more advanced embedded systems that allow various financial operations without personnel involvement. These devices combine the functionalities of ATMs, cash deposit machines, and even multimedia terminals, making them versatile and appealing to customers.

User Interface: Embedded systems enable intuitive operation with touch interfaces and automatic personalization. The embedded software remembers user preferences, allowing customization of the user experience to individual needs, such as loyalty card support or financial offers.

Transactional Modules: In self-service financial terminals, embedded systems facilitate various transactions, such as bill accepting payments, money transfers, insurance purchases, or mobile top-ups. Integrated communication modules synchronize transactions with central banking servers, ensuring instant operation approval.

Information Management Systems: Thanks to embedded systems, financial terminals can analyze transaction data and transmit it to banks in real-time. This enables better monitoring of operations and customer behavior analysis, which in turn supports service optimization.

Advanced Payment Processing: Integrating IoT and Smart Sensors

Moreover, IoT devices and smart sensors equipped with embedded systems are used to monitor the value of assets that serve as loan collateral, such as leased machinery or real estate. These systems collect data on the technical condition and location of collateral assets, enabling traditional financial institutions to assess the risk associated with individual assets.Example: In the leasing of machinery or commercial vehicles, embedded systems track their location, technical condition, and usage intensity. This information can be automatically transmitted to risk management systems, allowing banks and leasing companies to dynamically adjust credit or collateral conditions based on the current state of the assets.Predictive Software: Based on sensor data, embedded systems can predict potential failures or maintenance needs. This helps minimize the risk of asset depreciation and optimizes maintenance schedules, which is valuable in managing credit risk.

ATM and Financial Point Monitoring: Smart sensors can monitor the physical environment of ATMs, detecting unauthorized access attempts, tampering, or skimming (card data theft). For example, motion sensors and accelerometers embedded in ATMs can send alerts to headquarters when they detect suspicious movements, suggesting a potential theft attempt.

Threat Detection Systems: Security sensors can identify threats such as attempts to open the ATM, physical vibrations, or sudden movements around the device. Embedded systems analyze these signals and can automatically trigger security procedures, such as locking access to the device or initiating an alert to security services.

Remote Updates and Diagnostics: Embedded systems allow for remote management of device software, enabling updates without the need for physical access to the machine. Banks can remotely monitor device status, identify issues, and perform diagnostics, increasing operational efficiency.

Energy Consumption Monitoring: IoT devices can also manage energy usage by switching devices to energy-saving mode or turning them off during idle periods. Remote management optimizes resource consumption and extends equipment lifespan, which is crucial for managing a large number of distributed devices.

Exploring the Role of Embedded Technology in Blockchain Data Storage and Security

Blockchain relies on a decentralized database that stores transaction information in immutable blocks. Embedded systems play a crucial role in the secure storage and real-time processing of this data, which is essential for maintaining transaction integrity and transparency.

Local Storage of Blockchain Fragments: In fintech devices such as POS terminals or ATMs, embedded systems can store fragments of the blockchain or transaction hashes. This enables these devices to verify transaction authenticity without needing access to a central server.

Decentralized Data Processing: Embedded systems support data processing in a peer-to-peer model, increasing efficiency and reducing costs associated with sending data to central servers. Decentralized processing also enhances resilience against attacks and infrastructure failures.

Data Tamper Protection: By employing cryptographic hashing functions, embedded systems can protect the blockchain against tampering. Each transaction or change in the blockchain is safeguarded by a unique hash, which prevents data modification without the consent of all parties.

Private Key Management: Private keys are used to authorize transactions on the blockchain. Embedded systems equipped with Hardware Security Modules (HSM) provide secure storage for these keys, minimizing the risk of theft or unauthorized access to blockchain accounts.

Advanced Encryption Mechanisms: Embedded systems utilize advanced encryption algorithms, such as AES-256, to protect data stored and processed on devices. This provides an additional layer of security against cyberattacks and tampering with blockchain data.

The Impact of Embedded Systems on Testing Types in the Fintech Industry

Testing embedded systems within the fintech sector require advanced and varied methods capable of meeting the unique demands of financial services, including reliability, security, and regulatory compliance. Below are some of the significant types of tests used in fintech and their roles in ensuring top quality and security for financial technology.a. Functional TestingFunctional testing in fintech applications is a foundational step to ensure that every system function operates as expected, free of errors. This type of testing focuses on the accuracy and reliability of essential features like transaction processing, authentication, and integration with external payment systems.

Automation: Due to the repetitive nature of certain operations, functional tests are often automated, enabling faster and more effective error elimination. For functional test automation in fintech, tools are used that not only test but also log every system change, enabling a more precise analysis of results.

b. Performance and Load TestingFintech systems must maintain high performance and stability even under heavy load, which is especially critical during peak times such as market openings or holiday periods. Performance and load testing allow teams to assess system behavior under different levels of demand.

Load Testing: Load testing evaluates the system’s ability to handle expected levels of demand, crucial for systems that need to accommodate thousands of users simultaneously.

Stress Testing: Stress testing simulates extreme conditions, such as mass withdrawals or cryptocurrency transactions, to gauge system resilience under high load and ensure it can recover smoothly after overload.

c. Security TestingFintech systems are frequent targets of cyberattacks, making security testing a critical component in development and maintenance. Security is paramount, and these tests aim to identify and resolve any vulnerabilities before they can be exploited.

Penetration Testing: Penetration testing simulates attacks on the system to identify any unpatched security gaps. Security teams use hacking techniques to ensure the system remains secure.

Data Encryption Testing: This testing ensures that all confidential data is properly encrypted both during transmission and storage. Advanced encryption algorithms, like AES-256, are commonly used in fintech to minimize the risk of data theft.

Authentication and Authorization Testing: This testing verifies that authentication protocols like two-factor authentication (2FA) function correctly. Multi-factor authentication is a crucial security measure in fintech, protecting against unauthorized access.

d. Compliance TestingCompliance with legal and industry regulations is essential in fintech, which is subject to strict rules, such as anti-money laundering (AML) and know-your-customer (KYC) requirements. Non-compliance can lead to costly penalties and reputational damage.

Compliance testing aims to verify that each update and deployment adheres to current legal regulations. It also includes checking fraud prevention mechanisms and protocols for securely storing customer data.

e. Regression TestingIn fintech systems, every update, bug fix, or new feature requires thorough testing to ensure that it doesn’t introduce new errors. Regression testing is particularly crucial, as any change in a complex embedded system can impact its stability and reliability.

Automating Regression Testing: In fintech, automating regression testing is essential due to the many integrated functions and security protocols. Automation tools enable rapid regression testing after each update, helping speed up the deployment of new features.

f. Reliability and Stability TestingReliability is a vital aspect of fintech systems, especially for ATMs, mobile payment points, and other self-service devices that require uninterrupted availability 24/7. Stability testing verifies the system's ability to operate continuously without failure.

Stability Analysis: Reliability testing assesses the system’s stability under various environmental conditions and variable loads. This is crucial in fintech, where any system downtime can lead to financial losses and decreased customer trust.

Long-Term Testing: Conducting long-term stability testing helps identify any minor issues that could grow and lead to system failures over time.

More about quality attributes in embedded systems you can read in our article:https://intechhouse.com/blog/quality-attributes-in-embedded-systems-how-to-build-reliable-and-resilient-devices/

The Future of Embedded Systems in Fintech: Key Trends to Watch

Embedded systems in the fintech sector are becoming increasingly advanced, responding to growing demands for security, efficiency, and scalability within financial services. One of the emerging trends is edge computing. In the financial sector, where every millisecond counts, edge computing allows operations and data processing to occur directly on the device, such as an ATM or a payment terminal, reducing dependency on network connectivity and minimizing latency. This solution is essential for improving transaction response times and optimizing the costs associated with transferring and processing large volumes of data in the cloud.Cybersecurity in embedded systems remains an absolute priority, especially given the rise in cyberattacks targeting the financial services. New embedded solutions are increasingly leveraging end-to-end encryption directly at the device level to protect user data from tampering. The use of homomorphic encryption and secure boot technology is becoming more widespread, ensuring software integrity at the embedded level. With secure boot, devices can only start up with trusted, authorized components, reducing the risk of running malicious software.Digital identity, enabling users to authenticate securely and seamlessly, is another crucial aspect of future systems. These embedded finance solutions require support from advanced biometric methods, such as facial recognition and fingerprint analysis, which are integrated directly into devices like POS systems and self-service terminalss. The high level of security in these systems is achieved through dedicated security processors that not only handle biometric data but also provide complete isolation for authentication data, ensuring a robust security framework.

InTechHouse: Your Partner in the Future of Embedded Fintech and Beyond

The future of fintech, powered by the development of embedded systems, looks promising. Following this path, it has the potential to improve the daily lives of millions by introducing technologies that make finance more accessible, intuitive, and trustworthy. From both present and future perspectives, the role of quality and testing will be the foundation of the industry’s continued success, driving innovation and ensuring a world where finance becomes even smarter and more secure.

InTechHouse is a company that not only specializes in embedded systems but also offers a wide range of technology services tailored to the needs of modern businesses. With a team of experienced engineers and experts from various fields, InTechHouse supports clients throughout the entire lifecycle of creating innovative products – from software design and IoT solutions to advanced mobile and web applications.We prioritize a comprehensive approach that also includes technology consulting, market analysis, and process optimization, allowing us to help your business fully harness the potential of digital transformation. Contact us to discover how we can achieve your technology goals together!

FAQ

What are the benefits of test automation in fintech systems?Test automation speeds up the testing process, allowing for faster error detection and reducing the time needed to introduce new features. Automated tests are more efficient, enabling more frequent testing and quick adaptation to changes, which is crucial in the dynamic fintech environment.Is testing in fintech expensive? Should costs be reduced?Testing in fintech is costly, but these expenses are minimal compared to potential losses from errors. Sometimes a minor oversight can cost millions, so investment in testing, especially in critical areas like security, is absolutely worthwhile.What are the most common errors detected when testing embedded systems in fintech?The most frequently detected issues are compatibility problems with other systems, data encryption errors, user authorization issues, and performance vulnerabilities under high traffic loads. Eliminating such errors is essential to avoid disruptions and potential risks.Can fintech use open-source tools for testing embedded systems, or is it too risky?Fintech companies often utilize open-source tools but add additional layers of security and audits to minimize risk. Testing with open-source solutions requires specific security procedures, but it can be effective and reduce operational costs.